- Home

- SMA’s Guide to Outsourcing Your Core System

A comprehensive guide to outsourcing your core... and more

Introduction: how to outsource your core

Outsourcing, upgrading, or migrating your core system is no small task — or quick decision. But it can be critical to the ongoing vitality of your financial institution (FI).

Clients and members depend on the streamlined financial services your core supports. But as their needs and wants evolve, you’ll need a core that is agile and allows the advanced features they expect, whether it’s real-time balances in your app, the ability to turn a card off if lost, mobile deposit, or third-party integrations with other apps they use regularly.

Implementing innovative new services to serve member and customer needs while still maintaining current operations can be quite a challenge. Coupled with the current trend in workforce shortages and the fact that many legacy systems are a significant obstacle to digital innovation, it is obvious why many financial institutions are outsourcing their core and more.

By turning over the reins to a core provider, FIs of all sizes can provide innovative services without overburdening IT staff with their management and deployment. This shift in responsibility allows your in-house team to focus on ways to better serve members and clients so you can retain and grow market share in a highly competitive market. But, as many financial institutions have realized, outsourcing operations to a core provider is not without its own set of risks.

So whether your organization is in the consideration stage or is already outsourcing its core system, the question remains: How do you maximize the benefits of outsourcing at every level, while minimizing the risk involved? Our comprehensive guide provides actionable insights and best practices for outsourcing to ensure your core partnership promotes operational control, increased efficiency, and reduced risk.

Outsourcing contents

- Outsourcing overview: Getting to the core of the matter

- When and why to outsource: Exploring migration patterns

- The risk is real: Is resistance futile?

- Mitigate risks with automation: Go with the flow

- Maximize the value of outsourcing

- Provider selection: Exploring core outsourcing providers

- Provider directory

- Additional resources

- Final considerations: The core of the matter

- FAQ

Outsourcing strategy: Getting to the core of the matter

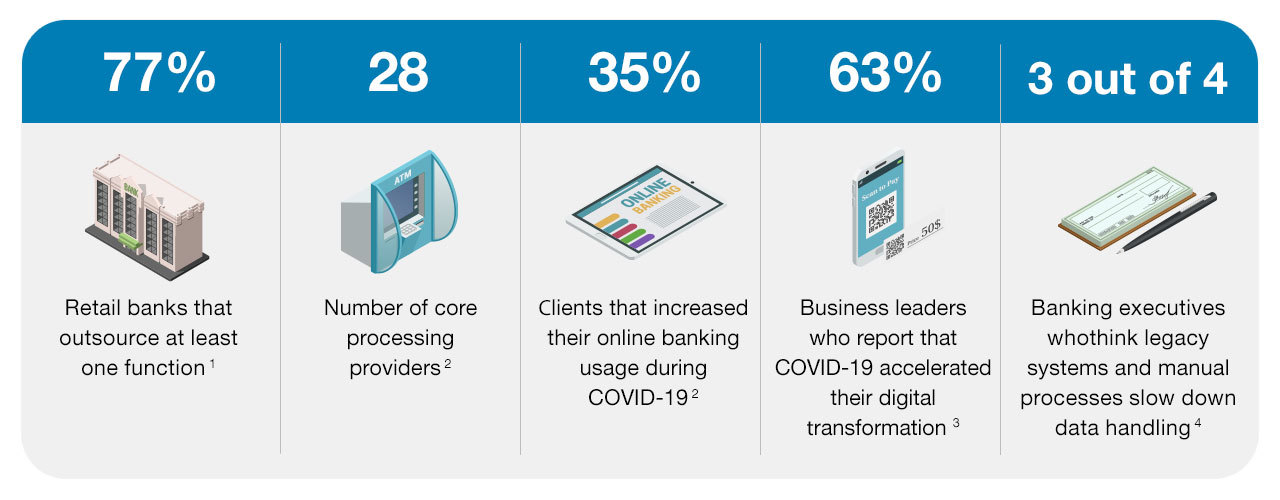

The best core system is one your clients or members never notice. Why? Because they only notice when the crucial infrastructure that maintains the banking platform fails, such as when deposits don’t post on time or balances don’t update. When the core is working, all your members and clients know is they can effortlessly deposit a check using their phone, transfer funds, or quickly apply for a car loan online.

Staff, however, have different needs for their core processing solution. One of the great benefits of keeping the system in-house is control. When the data is on-premises, IT staff and executives can confidently manage processes and timelines, see the data when they need to, and make changes to allow their other systems to interface with the core as needed. Outsourcing can seem risky, as data and processes move off-site and out of the FI’s direct control.

How do you help maintain that environment where everything just works? Many FIs have chosen to outsource core and IT processes, especially as consumer demand for non-contact options grew during the COVID-19 pandemic.

Of course, core processing isn’t the only option when it comes to outsourcing. Other tasks commonly outsourced by FIs include:

Data Management

Security

Identity verification

Loan processing

Disaster recovery

App development

With a wide variety of core processing providers of different sizes, credit unions and banks are able to create a blended environment that not only meets the needs of staff, but clients or members as well.

When and why to outsource: Exploring migration patterns

While some financial institutions are able to manage a nimble core processor in-house, many don’t have the staffing or budget to take on the development and maintenance themselves. That’s when outsourcing to a white-label core processing provider makes sense.

If you currently outsource your core or are considering the option, you undoubtedly encountered some significant operational pain at some point. But in most cases, it isn’t one service-related event or back office challenge, but a series of unfortunate experiences that led to the desire to outsource your core processing.

Common scenarios that lead to outsourcing a core system include:

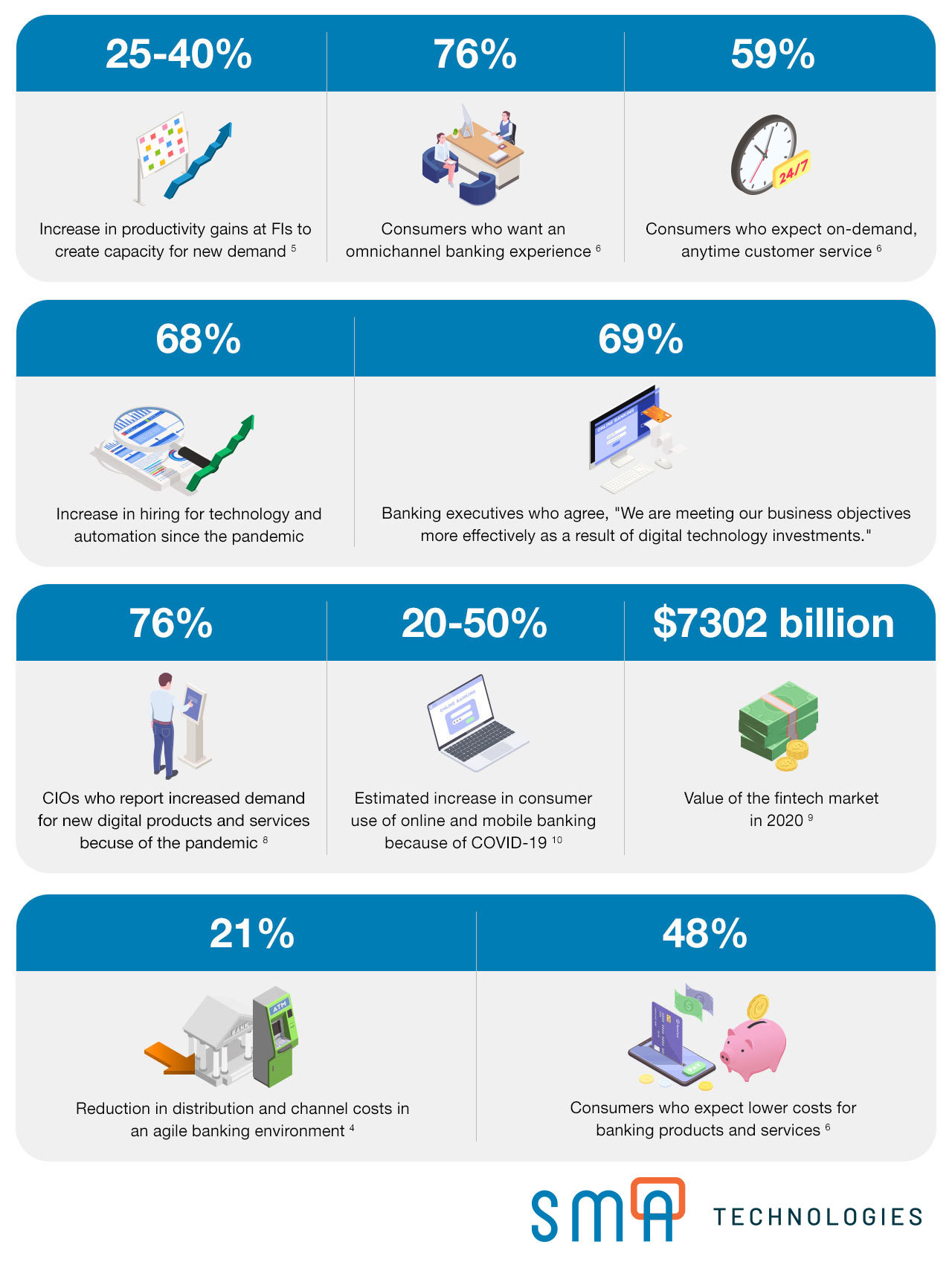

Outsourcing core processing can help solve these and other issues. And FIs typically find other benefits once they begin outsourcing services, especially in the area of member and customer service delivery in a post-pandemic world.

Consumer Needs Are Driving Digital Transformation for Financial Institutions

7 benefits of outsourcing for financial institutions

Streamlined and secure banking operations: Outsourcing provides less down time because of operational redundancies and high-level security features baked into most core processors.

More efficient use of resources: IT staff no longer has to work nights and weekends to apply patches and upgrades to systems. Managers are freed from day-to-day core maintenance to focus on strategic in-house initiatives.

Ability to innovate: FIs can develop digital growth strategies in-house or partner with core-compliant third parties to deploy market leading tools to better serve members

Regulatory compliance: Access to full regulatory and policy compliance reporting tools.

Business continuity: Robust backups and uptime ensures continuity of service and foolproof disaster recovery methods.

Management of workforce risks: With the right approach to outsourcing, processes can be documented to mitigate against risk of the loss of institutional knowledge as a result of staff turnover.

- Cost savings: By saving money on investments in hardware, software, and certain IT positions, banks and credit unions can reallocate resources. Outsourcing also allows FIs to manage core data processing as an operational expense rather than a capital investment.

Why financial institutions resist outsourcing

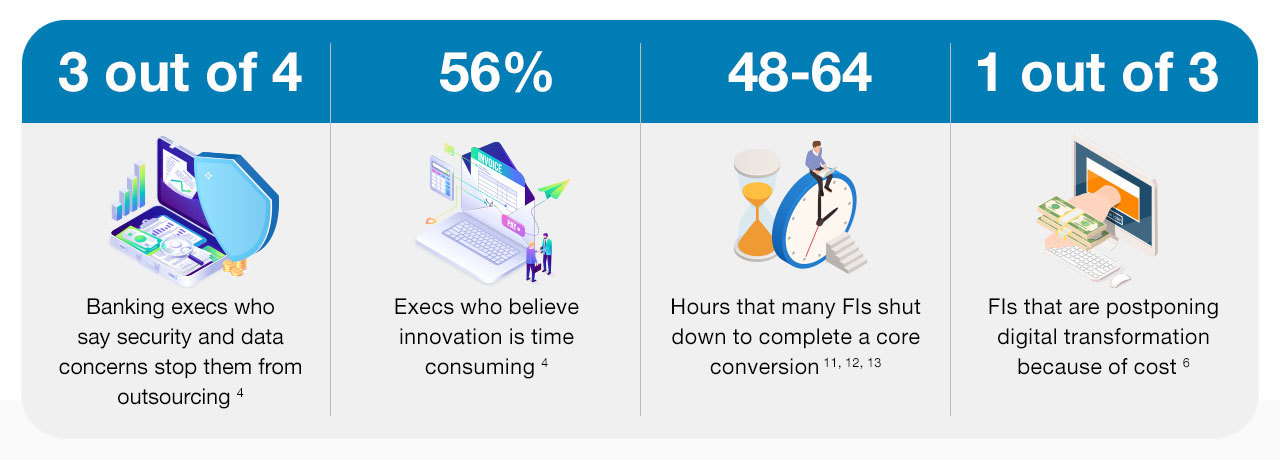

Although outsourcing a core system has numerous benefits, there can be an element of risk. Even though outsourcing can allow FIs to be more agile and responsive to consumer needs, many continue to put off outsourcing because of the potential pitfalls involved. Weighing the benefits of outsourcing against the risks is an important consideration for financial institutions.

Mitigate risks with automation: Go with the flow

Loss of Control

One of the biggest concerns among FIs considering outsourcing is the loss of control when your processing moves out of house. What is the recovery process if the system goes down? How can your team integrate new tools into the core when it’s not managed in-house? And who will ensure that your team has access to the data they need when they need it?

When your core is managed in-house, you know the answers to these questions and can shift priorities quickly when needed.

Consider this . . . Maintaining staff during non-business hours is costly and distracts internal resources when new strategic initiatives need to be undertaken.

Loss of Visibility

Would you get in the car with someone who told you they’d get you where you’re going really fast, but you have to wear a blindfold the entire way? Maybe, but you’d probably feel uneasy. And that can be what it feels like to outsource your core processes.

You can see that processes occur, but you don’t necessarily have visibility of the timing or duration. That can be a stark contrast to when your core is in-house, and you’re able to set your own schedule, detect and address errors along the way, and make adjustments necessary to accommodate your internal needs.

Consider this . . . When managing processes in-house, scheduling around regular operations can be challenging, not to mention burdensome for internal staff.

Data Security

When data is stored on your servers, your staff maintains control of security procedures to safeguard member and client information. Sending data to cloud-based servers or outside networks involves additional risks outside your control. And when those servers are overseas, the risk of lax security procedures and lack of enforcement authority can make outsourcing seem even more dangerous.

Consider this . . . Data stored in-house is by no means impervious to hacks, social engineering, or other security breaches. Outsourcing can eliminate your IT staff's struggle to identify risks and manage security patch updates while managing other day-to-day issues.

Service Interruptions

Service interruptions are a real risk when processing is outsourced. Beyond the downtime involved in the initial transfer of data, there is the risk that servers will fail or the network will drop, and FIs have little control over how they are brought back online.

Consider this . . . Hardware and software failures are a risk with an in-house core as well. And outsourcing can add levels of redundancy that are challenging for many FIs to maintain on their own to ensure business continuity.

Loss of Institutional Knowledge

When you outsource processes to third parties, FI staff may forfeit valuable institutional knowledge about processing task scheduling, parameters, workflows, and more.

Consider this . . . Outsourcing to a third party can mitigate the risk of essential staff leaving and taking all of their knowledge with them, and replacing staff can be easier when they don’t need the specialized knowledge necessary to manage an in-house fully proprietary core.

Workload Automation and Outsourcing

At a basic level, workload automation is the process of automating routine and time-consuming manual processes. An automation platform uses software to schedule, initiate, and execute processes as defined by the user. More than just a batch scheduler, however, a robust automation platform offers financial institutions the flexibility to create self-service workflows, deploy server updates, and monitor an entire system from a single user interface.

Although automation offers benefits for FIs separate and apart from the outsourcing process, because of its features and functionality, a robust automation platform can provide the safety net FIs need when outsourcing their core system. And for those FIs that have already outsourced, automation can help them maximize the benefits of outsourcing in tangible ways.

SMA Technologies’ own workload automation and orchestration platform is called OpCon. For organizations considering outsourcing, SMA’s ops team can fully manage the outsourcing project so that your team can be redeployed to other strategic projects. Request a demo.

Digital transformation is challenging and can be expensive

Outsourcing and automation are the one-two punch that helps mitigate costs, reduce risks, and finally allow the level of innovation your clients or members need.

It’s also worth pointing out that workload automation and orchestration requires a minimal investment relative to the total costs involved with outsourcing to a third-party core provider. And the implementation can be relatively fast as well. Even in environments where outsourcing isn’t an option, workload automation is a crucial tool to improve organizational efficiency.

Read on to see why workload automation and orchestration is mission critical for financial institutions.

5 Ways automation maximizes the advantages of outsourcing

- Restore control: Outsourcing to a third party does not need to involve a complete relinquishment of control. An automation platform can monitor service level agreements (SLAs) and provide robust features for improving connections across an FIs application system, including the movement of files into and out of the core.

Maintain visibility: During and even after migrating their core, FIs can find it challenging to monitor processes and ensure that systems are operational. Workload automation and orchestration provides a real-time view of the entire system and allows all levels of the organization to work from a shared vision.

Manage services: As FIs strive to create an agile environment, it may be necessary to outsource more than just the core. The right automation tool can orchestrate numerous processes to provide enhanced functionality and seamless service to members and clients. And scalability is baked into automation so that, in most cases, adding new workflows, processes, and integrations won’t require increased staffing or the associated cost expenditures.

Enshrine institutional knowledge: , With the combined power of automation and outsourcing, an automation platform will preserve the vital knowledge of critical system processes and workflows, even when staff leaves or when processes move off-premises. FIs never have to worry that system processes will be lost because every step of the process will be automated and documented for easy retrieval at any time.

Free up staff to innovate: One of the most common benefits of outsourcing is that financial institutions can be more nimble and redirect internal resources to innovation initiatives. An automation platform has a multiplier effect on this benefit. One of our clients reported that they were able to reduce and redeploy staff hours by 1,000 per year after implementing our tool. Other clients have also found that they reduced errors by 90% by automating processes. When your team isn’t spending time on repetitive processes that drain resources, they can focus on strategic initiatives to accelerate your digital transformation and move your organization forward.

Process outsourcing to the right provider: Exploring core outsourcing providers

As you investigate potential core processing providers, you’ll need to investigate what they offer, how well they integrate with your other systems, and whether they will fit your overall needs.

The first step will be creating a cross-departmental team to oversee the outsourcing project, define the specific desired outcomes, and advise on the final selection of a vendor. Be sure that all relevant departments of the FI are represented: executives, IT, marketing, research, finance, and front-line staff. IT leadership should anchor the process and be given a voice in conversations related to the strategic direction of your FI.

Then look at the different vendor options and the products they offer. Read the product descriptions to see what features they offer. Explore their blogs and case studies. Review testimonials. See below for a directory of vendors.

During the initial exploration phase, you can narrow down a list of vendors to explore further. Consider assigning a subcommittee to handle this task while another subgroup takes on the next. Once you’ve got your shortlist, create a list of criteria with input from all departments in your FI. A rubric will help all members of the committee assess and discuss the viable options within a framework that defines your organizational objectives for the project.

Contact the vendors on your shortlist to get more targeted information, schedule demos for your team, and request pricing and contract terms. Also, ask for customer contacts you can speak with to get targeted information. However, don’t simply depend on the contacts the vendor gives you. Reach out to other financial institutions for their unvarnished opinions.

Following is an evaluative framework that can help guide you through the process of selecting a provider for outsourcing your core.

Criteria to assess when evaluating core providers for your outsourcing strategy

Expand the content below to learn more about each.

First, you’ll want to list your primary objectives or desired outcomes for the outsourcing project.

First, you’ll want to list your primary objectives or desired outcomes for the outsourcing project.

Although pricing should not be the main criterion, comparing pricing at the outset can ensure that all the vendors you explore will fit within your budget.

• How does pricing change for your asset size and number of members or customers?

• How is pricing impacted as your business scales?

• Are there varied feature sets that affect pricing?

Although pricing should not be the main criterion, comparing pricing at the outset can ensure that all the vendors you explore will fit within your budget.

• How does pricing change for your asset size and number of members or customers?

• How is pricing impacted as your business scales?

• Are there varied feature sets that affect pricing?

Explore how well the core product fits your organization’s requirements.

• Does the system include the processes and functionalities you need?

• How many of your banking processes can be handled by the core processing products and the vendor’s related products?

• In your research with their current clients, does their service level meet the expectations you have for vendor support?

Explore how well the core product fits your organization’s requirements.

• Does the system include the processes and functionalities you need?

• How many of your banking processes can be handled by the core processing products and the vendor’s related products?

• In your research with their current clients, does their service level meet the expectations you have for vendor support?

Assess how well the core processing solution integrates with the internal and third-party tools you already use.

• Is the core compatible with your must-have third-party plugins?

• If not, can you switch to other third-party tools that are compatible? If so, do you have the bandwidth to handle multiple conversions at once?

• Does the core encompass some of the processes you’re currently using third-party or specialized tools to manage?

• Does the core offer an API so you or other vendors can add new functionalities?

Assess how well the core processing solution integrates with the internal and third-party tools you already use.

• Is the core compatible with your must-have third-party plugins?

• If not, can you switch to other third-party tools that are compatible? If so, do you have the bandwidth to handle multiple conversions at once?

• Does the core encompass some of the processes you’re currently using third-party or specialized tools to manage?

• Does the core offer an API so you or other vendors can add new functionalities?

As you investigate core processing vendors, you’ll find they tend to specialize in FIs of a certain size, such as credit unions over $1 billion in assets or community banks between $250-500 million.

• What FI profiles are most commonly served by the vendor?

• If the vendor serves your size FI, do they have the capacity to scale with you as you grow?

As you investigate core processing vendors, you’ll find they tend to specialize in FIs of a certain size, such as credit unions over $1 billion in assets or community banks between $250-500 million.

• What FI profiles are most commonly served by the vendor?

• If the vendor serves your size FI, do they have the capacity to scale with you as you grow?

As you assess the various contracts, keep in mind that some terms can be negotiated for more favorable outcomes for your FI.

• How long is the contract?

• What is the process if either party needs to terminate early?

• Who is liable if problems occur, either during the migration itself or afterward?

• What is the deconversion process if you choose to migrate to another core processor in the future?

As you assess the various contracts, keep in mind that some terms can be negotiated for more favorable outcomes for your FI.

• How long is the contract?

• What is the process if either party needs to terminate early?

• Who is liable if problems occur, either during the migration itself or afterward?

• What is the deconversion process if you choose to migrate to another core processor in the future?

As your needs (and your member and client needs!) evolve, consider whether the vendor is suited to provide ongoing strategic support.

• What features are on the product roadmap?

• How are new features and functionalities rolled out?

• What level of input do customers have on the product roadmap and expansion plans?

• What do current customers say about how well the core can adapt to the changes in their FI?

As your needs (and your member and client needs!) evolve, consider whether the vendor is suited to provide ongoing strategic support.

• What features are on the product roadmap?

• How are new features and functionalities rolled out?

• What level of input do customers have on the product roadmap and expansion plans?

• What do current customers say about how well the core can adapt to the changes in their FI?

Before selecting a vendor, assess their reputation for providing stellar support during the conversion and for offering solid ongoing support.

• What support does the vendor provide during conversion?

• If something goes wrong, how will you be notified and what steps will be taken?

• What service is included in the standard contract? Are there options to upgrade service levels should the need arise?

• How is uptime measured, and does the vendor offer uptime guarantees?

• What remedies are available if the vendor does not meet service promises or uptime guarantees?

Before selecting a vendor, assess their reputation for providing stellar support during the conversion and for offering solid ongoing support.

• What support does the vendor provide during conversion?

• If something goes wrong, how will you be notified and what steps will be taken?

• What service is included in the standard contract? Are there options to upgrade service levels should the need arise?

• How is uptime measured, and does the vendor offer uptime guarantees?

• What remedies are available if the vendor does not meet service promises or uptime guarantees?

An engagement with a core processing vendor should be considered a long-term relationship in most cases. When vetting vendors, ensure that they have the history and stability to be a viable solution.

• Are they financially stable?

• How long has the vendor been providing core processing to FIs?

• What other services do they provide, and how many FIs do they currently serve?

• Are they likely to be acquired in the future, should that occur, how will your contract be managed?

An engagement with a core processing vendor should be considered a long-term relationship in most cases. When vetting vendors, ensure that they have the history and stability to be a viable solution.

• Are they financially stable?

• How long has the vendor been providing core processing to FIs?

• What other services do they provide, and how many FIs do they currently serve?

• Are they likely to be acquired in the future, should that occur, how will your contract be managed?

Provider directory

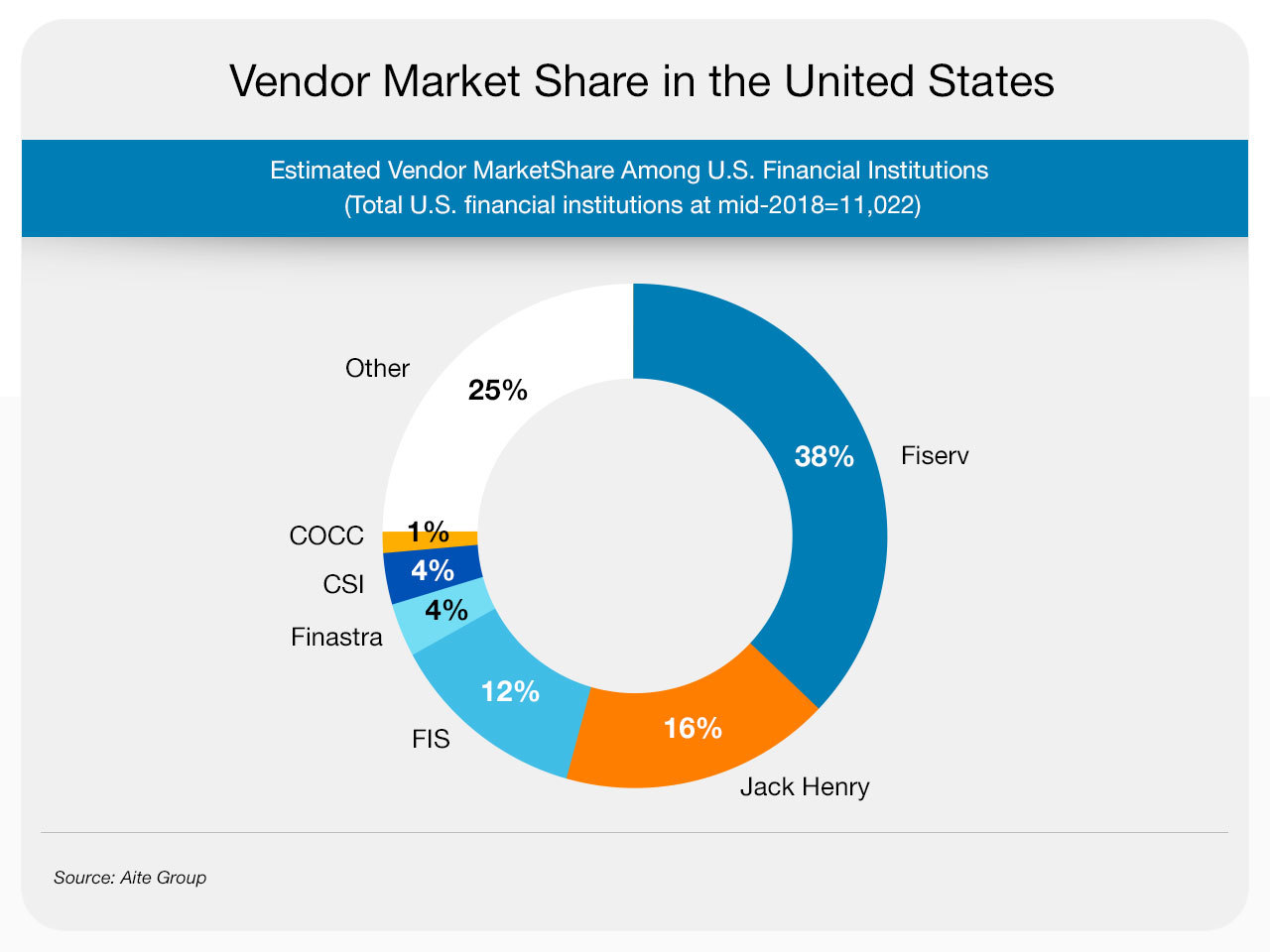

The core processing market is fairly lopsided in that a few big players serve the lion’s share of financial institutions.

In all, there 28 core processing vendors. The following alphabetized directory offers a selection of some of the largest core processing vendors.

Vendors for outsourcing core processing

Click into each of the vendors below to learn more about each.

COCC’s core solution is an open Oracle database using a Windows-based .NET architecture. They offer pre-built integrations and use their open core technology to ensure ease of upgrades and integrations. Other services include data management, lending, and marketing.

COCC’s core technology enables us to integrate best-of-breed ancillary products to the core. Because we use the latest technologies, our integration processes are simpler and more complete than legacy systems. This enables us to “shop” for the new and innovative products to improve a financial institution’s capabilities and offer choices to meet each client’s needs. Source: CCOC

• Phone: 860-678-0444

COCC’s core solution is an open Oracle database using a Windows-based .NET architecture. They offer pre-built integrations and use their open core technology to ensure ease of upgrades and integrations. Other services include data management, lending, and marketing.

COCC’s core technology enables us to integrate best-of-breed ancillary products to the core. Because we use the latest technologies, our integration processes are simpler and more complete than legacy systems. This enables us to “shop” for the new and innovative products to improve a financial institution’s capabilities and offer choices to meet each client’s needs. Source: CCOC

• Phone: 860-678-0444

Corelation’s core processing system is Keystone. They feature KeyBridge, an open API, to allow customization and integrations with a wide variety of third-party tools.

Our KeyStone core solution leverages state-of-the-art architecture with the bold goal of transforming the way credit unions operate. KeyStone features a person-centric design, intuitive display, open architecture, and the most advanced programming tools available. Developed by a system architect with more than 40 years of experience creating successful core processing solutions for credit unions, KeyStone serves the complex needs of credit unions today while positioning them for the changing needs of tomorrow. Source: Corelation

Phone: 619-876-5074

Email: [email protected]

Website: https://corelationinc.com/

Corelation’s core processing system is Keystone. They feature KeyBridge, an open API, to allow customization and integrations with a wide variety of third-party tools.

Our KeyStone core solution leverages state-of-the-art architecture with the bold goal of transforming the way credit unions operate. KeyStone features a person-centric design, intuitive display, open architecture, and the most advanced programming tools available. Developed by a system architect with more than 40 years of experience creating successful core processing solutions for credit unions, KeyStone serves the complex needs of credit unions today while positioning them for the changing needs of tomorrow. Source: Corelation

Phone: 619-876-5074

Email: [email protected]

Website: https://corelationinc.com/

CSI’s core tools include NuPoint and Meridian. They also offer integrations and stand-alone tools for digital banking and cybersecurity.

CSI operates at the intersection of innovative technology solutions, uncompromising service and decades of experience. From digital transformation and regulatory compliance in banking to network security and sanctions screening in regulated industries, we are the experts behind today’s top fintech and regtech solutions. Source: CSI

Phone: 800-545-4274

Website: https://www.csiweb.com/

Contact form: https://www.csiweb.com/contact...

CSI’s core tools include NuPoint and Meridian. They also offer integrations and stand-alone tools for digital banking and cybersecurity.

CSI operates at the intersection of innovative technology solutions, uncompromising service and decades of experience. From digital transformation and regulatory compliance in banking to network security and sanctions screening in regulated industries, we are the experts behind today’s top fintech and regtech solutions. Source: CSI

Phone: 800-545-4274

Website: https://www.csiweb.com/

Contact form: https://www.csiweb.com/contact...

FedComp offers four different levels of their Platinum core processing solution to serve FIs of different asset sizes.

For more than 35 years FedComp has serviced its credit union clients’ core data processing needs, both technically and with live 24/7 customer support. FedComp is a leading Microsoft-based core processing system, evolving from DOS in 1982 to Windows 10 today. Since 1984, more than 3,500 credit unions have employed its core data system. Today $3.8 billion in assets are managed by FedComp with credit unions in the continental U.S., Caribbean and the United Kingdom. Source: FedComp

Phone: 800-733-3266

Website: https://www.fedcomp.com/

Contact form: https://www.fedcomp.com/web-re...

FedComp offers four different levels of their Platinum core processing solution to serve FIs of different asset sizes.

For more than 35 years FedComp has serviced its credit union clients’ core data processing needs, both technically and with live 24/7 customer support. FedComp is a leading Microsoft-based core processing system, evolving from DOS in 1982 to Windows 10 today. Since 1984, more than 3,500 credit unions have employed its core data system. Today $3.8 billion in assets are managed by FedComp with credit unions in the continental U.S., Caribbean and the United Kingdom. Source: FedComp

Phone: 800-733-3266

Website: https://www.fedcomp.com/

Contact form: https://www.fedcomp.com/web-re...

Finastra’s Fusion Phoenix platform can integrate with their portfolio of tools for lending and commercial banking.

Finastra offers the most comprehensive portfolio of end-to-end lending solutions in the market – across syndicated, commercial, consumer, and mortgage lending.

We deliver a consistent, frictionless digital borrower experience for a range of businesses, corporations and consumers, whilst improving customer onboarding, increasing transparency and streamlining back-office operations.

As well as reducing complexity, cost and manual processes, Finastra’s solutions provide a single platform to deliver efficiency and a clear return on investment. Source: Finastra

Phone: 800-989-9009

Website: https://www.finastra.com/

Contact form: https://www.finastra.com/conta...

Finastra’s Fusion Phoenix platform can integrate with their portfolio of tools for lending and commercial banking.

Finastra offers the most comprehensive portfolio of end-to-end lending solutions in the market – across syndicated, commercial, consumer, and mortgage lending.

We deliver a consistent, frictionless digital borrower experience for a range of businesses, corporations and consumers, whilst improving customer onboarding, increasing transparency and streamlining back-office operations.

As well as reducing complexity, cost and manual processes, Finastra’s solutions provide a single platform to deliver efficiency and a clear return on investment. Source: Finastra

Phone: 800-989-9009

Website: https://www.finastra.com/

Contact form: https://www.finastra.com/conta...

Finxact’s core system is cloud-based. Rather than offering a set of predesigned integrations, they use a series of partners to help create integrations.

Finxact uniquely delivers a cloud-native Core as a Service, enabling fast, streamlined innovation without technology upheaval. Build, design and rapidly bring to market new products and services, how and when you want.

Finxact partners with leading systems integrators that help banks design and execute their core transformation strategies. Source: Finxact

Phone: 866-834-6922

Email: [email protected]

Website: https://finxact.com/

Contact form: https://finxact.com/contact-us...

Finxact’s core system is cloud-based. Rather than offering a set of predesigned integrations, they use a series of partners to help create integrations.

Finxact uniquely delivers a cloud-native Core as a Service, enabling fast, streamlined innovation without technology upheaval. Build, design and rapidly bring to market new products and services, how and when you want.

Finxact partners with leading systems integrators that help banks design and execute their core transformation strategies. Source: Finxact

Phone: 866-834-6922

Email: [email protected]

Website: https://finxact.com/

Contact form: https://finxact.com/contact-us...

FIS offers the IBS, Horizon, Systematics, and Profile core processors. They also have products for lending, payments, commercial banking, and more.

FIS is passionate about giving back to our 3 C’s — Colleagues, Clients and Communities — and working to ensure no one is left behind.

FIS stays ahead of how the world is evolving to power businesses, across merchants, banking and capital markets, to outpace today’s fast-changing competitive landscape and help our clients run, grow and achieve more for their business. Source: FIS

Phone: 877-776-3706

Email: [email protected]

Website: https://www.fisglobal.com/

FIS offers the IBS, Horizon, Systematics, and Profile core processors. They also have products for lending, payments, commercial banking, and more.

FIS is passionate about giving back to our 3 C’s — Colleagues, Clients and Communities — and working to ensure no one is left behind.

FIS stays ahead of how the world is evolving to power businesses, across merchants, banking and capital markets, to outpace today’s fast-changing competitive landscape and help our clients run, grow and achieve more for their business. Source: FIS

Phone: 877-776-3706

Email: [email protected]

Website: https://www.fisglobal.com/

Fiserv has the largest market share among core providers serving FIs. It offers the DNA, Signature, ClearTouch, Precision, and Premier core processors, as well as a variety of other solutions to process payments, loans, and more

Fiserv enables money movement for thousands of financial institutions and millions of people and businesses in a world that never powers down.

Thousands of financial institutions rely on Fiserv to help them deliver essential financial services to their customers.

From account processing and a wide range of payment services, to solutions that enable them to mitigate and manage risk and more efficiently manage the channels through which their services are delivered, our clients look to Fiserv for innovative solutions and expertise. Source: Fiserv

Phone: 800-872-7882

Website: https://www.fiserv.com/

Contact form: https://www.fiserv.com/en/abou...

Fiserv has the largest market share among core providers serving FIs. It offers the DNA, Signature, ClearTouch, Precision, and Premier core processors, as well as a variety of other solutions to process payments, loans, and more

Fiserv enables money movement for thousands of financial institutions and millions of people and businesses in a world that never powers down.

Thousands of financial institutions rely on Fiserv to help them deliver essential financial services to their customers.

From account processing and a wide range of payment services, to solutions that enable them to mitigate and manage risk and more efficiently manage the channels through which their services are delivered, our clients look to Fiserv for innovative solutions and expertise. Source: Fiserv

Phone: 800-872-7882

Website: https://www.fiserv.com/

Contact form: https://www.fiserv.com/en/abou...

Jack Henry serves banks and credit unions through the SilverLake, CIF, CoreDirector, and Symitar core processing solutions. They also offer related products to process loans, cards, payments, and more.

JHA provides more than 300 products and services that enable our customers to process financial transactions, automate their businesses, and succeed in an increasingly competitive marketplace. Our three brands – Jack Henry Banking®, Symitar®, and ProfitStars® – support financial institutions of all sizes, diverse businesses outside the financial industry, and other technology providers.

“We understand that impeccable service starts with us, empowers our customer, and ultimately enhances the consumer experience. We serve the financial institution looking to simplify day-to-day processes. The college student who expects on-the-go account access. The small business owner searching for better tools to process payments. We all seek simple, accessible, consistent, and secure solutions for financial management. Source: Jack Henry

Phone: 417-235-6652

Website: https://www.jackhenry.com/

Contact Form: https://www.jackhenry.com/more...

Jack Henry serves banks and credit unions through the SilverLake, CIF, CoreDirector, and Symitar core processing solutions. They also offer related products to process loans, cards, payments, and more.

JHA provides more than 300 products and services that enable our customers to process financial transactions, automate their businesses, and succeed in an increasingly competitive marketplace. Our three brands – Jack Henry Banking®, Symitar®, and ProfitStars® – support financial institutions of all sizes, diverse businesses outside the financial industry, and other technology providers.

“We understand that impeccable service starts with us, empowers our customer, and ultimately enhances the consumer experience. We serve the financial institution looking to simplify day-to-day processes. The college student who expects on-the-go account access. The small business owner searching for better tools to process payments. We all seek simple, accessible, consistent, and secure solutions for financial management. Source: Jack Henry

Phone: 417-235-6652

Website: https://www.jackhenry.com/

Contact Form: https://www.jackhenry.com/more...

Nymbus’s core platform is cloud-based and has a variety of integratable digital, lending, and CRM tools.

Nymbus enables banks and credit unions of any size to accelerate growth through new routes to market. This includes a full suite of banking technology applications available to modernize and optimize existing channels, as well as the operational resources to get to market quickly with a full-scale digital bank immediately positioned at capturing new niche customer segments. Whichever growth path you choose, Nymbus buys back decades of lost time and accelerates your ability to engage and support the entire customer journey. Source: Nymbus

Phone: 855-210-7874

Website: https://www.nymbus.com/

Contact Form: https://www.nymbus.com/lp/cont...

Nymbus’s core platform is cloud-based and has a variety of integratable digital, lending, and CRM tools.

Nymbus enables banks and credit unions of any size to accelerate growth through new routes to market. This includes a full suite of banking technology applications available to modernize and optimize existing channels, as well as the operational resources to get to market quickly with a full-scale digital bank immediately positioned at capturing new niche customer segments. Whichever growth path you choose, Nymbus buys back decades of lost time and accelerates your ability to engage and support the entire customer journey. Source: Nymbus

Phone: 855-210-7874

Website: https://www.nymbus.com/

Contact Form: https://www.nymbus.com/lp/cont...

Additional resources

If you’d like to learn more about how to maximize the benefits of outsourcing your core, the resources below may be helpful for you:

The Case for Outsourcing

5 Questions That Reveal Whether Your Core Strategy Is Prepared for the Future (CUTimes.com)

- If you’re still on the fence about whether or not to outsource your core, use the five-question framework in this article to guide your team discussion and determine whether outsourcing is the right approach for your organization.

Thinking About Outsourcing Some of Your Operations? Make Sure You Plan Accordingly (NCUA)

- This report provides the steps to follow to ensure that your FI has a solid strategy for the shift from in-house to outsourced. One of the key pieces in this resource is information to guide your risk assessment of the potential core processing vendors. Although we’ve covered the risks and benefits here, the framework provided by NCUA will help you do a highly personalized risk assessment.

The 2021 CIO Agenda: Seize This Opportunity for Digital Business Acceleration (Gartner)

- Gartner offers a business case for outsourcing, from the CIO point of view. The report covers the prospective organizational benefit of reallocating the IT budget to foster innovation and agility. It also includes some interesting data on how digital transformation can benefit clients and members.

Vetting Potential Vendors

AIM Evaluation: The Leading Providers of U.S. Core Banking Systems (Aite-Novarica Group)

- Aite-Novarica Group provides an in-depth analysis of the core processing market and evaluates six of the top vendors. This report contains a lot of helpful information but, unfortunately, it’s not free. Contact Aite-Novarica Group for pricing information.

Core Systems Strategy for Banks (McKinsey & Company)

- McKinsey offers a helpful framework for deciding whether to use a private or public cloud for your core processor. Many core processing vendors currently rely on a public cloud. If you are considering this direction, McKinsey offers a framework you can use to assess whether your vendor meets your security requirements.

How to Avoid a Disaster When Switching Your Core Banking Platform (The Financial Brand)

- What do FIs often overlook when assessing core processing vendors? User experience. Because so much member and client demand is driving digital transformation in FIs, UX should be a critical element to explore when choosing vendors.

Incorporating Workload Automation and Orchestration

What Is Workload Automation? (SMA Technologies)

- We’ve already explained how workload automation and orchestration can help your FI maximize the benefits of outsourcing and minimize the risks. This article offers a more detailed explanation of what workload automation is and how it can help your organization.

Top 14 Workload Automation Use Cases in IT, HR, & Accounting (AIMultiple)

- This article offers specific use cases for workload automation in action. Although limited in scope, the tangible examples may be helpful.

Leverage Automation to Double IT Output, Not Staff (SMA Technologies)

- In this webinar, we cover real-work examples of how workload automation and orchestration can support your staff, free them up from repetitive tasks and increase employee morale and engagement.

Final outsourcing considerations: The core of the matter

Because your core system is such a vital part of your FI, making the right decision about whether and how to outsource to a third party can be daunting. And if you’ve already outsourced your core, it’s possible your organization has not yet fully realized the benefits of the arrangement.

Most vendors offer some type of add-on that can move data to and from the core, but it may not be fast enough or provide the levels of visibility and control you require. Remember, you don’t need to turn over the reins when you outsource your core. Maintain operational control by managing your tech stack with workload automation and orchestration.

Core + workload automation & orchestration: Your one-two punch for effective outsourcing

Workload automation and orchestration puts you in the driver’s seat when your outsource in five important ways:

Restore control when the core moves out of house.

Retain visibility of core processes.

Integrate processes and information across multiple outsourced and in-house systems.

Systematize and document tasks to ensure institutional knowledge stays in house.

Create an environment where staff have the time and resources to innovate.

At SMA Technologies, we leave nothing to chance when it comes to helping financial institutions navigate the visibility and control problems that can accompany outsourcing. We’ll have your back when you partner with an outsourcing provider to make sure that you can maximize the benefits of your relationship with your third-party vendor.

Frequently Asked Core Outsourcing Questions

Click on the questions below to see what others are often asking about outsourcing.

A: Any system that involves repetitive tasks and the potential for human error can benefit from workload automation and orchestration. The costs associated with this type of tool are usually modest compared to other technology outsourcing, meaning ROI is quickly realized.

A: Any system that involves repetitive tasks and the potential for human error can benefit from workload automation and orchestration. The costs associated with this type of tool are usually modest compared to other technology outsourcing, meaning ROI is quickly realized.

A: Open communication is critical with this or any other major undertaking. Speak about why you need to outsource, the benefits to the members or clients, and how it will make staff jobs easier. Listen to their concerns and respond honestly. It is likely that they feel the same pain points, so if you present the core conversion as the best solution to those problems, it should be easy to get everyone on board. When undertaken in the right context and approached strategically, outsourcing your core system can free up your IT staff to be more involved in the strategic direction of your organization.

A: Open communication is critical with this or any other major undertaking. Speak about why you need to outsource, the benefits to the members or clients, and how it will make staff jobs easier. Listen to their concerns and respond honestly. It is likely that they feel the same pain points, so if you present the core conversion as the best solution to those problems, it should be easy to get everyone on board. When undertaken in the right context and approached strategically, outsourcing your core system can free up your IT staff to be more involved in the strategic direction of your organization.

A: Checking references for a vendor is a lot like checking references for a potential hire. Create a list of common questions to ensure that all reference checks cover the same information. Important topics to cover include security, how the relationship works between your staff and the support team at the core processing vendor, how they would describe their core conversion experience, what they learned in the process, what they’d do differently next time, and what they wish they had asked when they were choosing a vendor.

A: Checking references for a vendor is a lot like checking references for a potential hire. Create a list of common questions to ensure that all reference checks cover the same information. Important topics to cover include security, how the relationship works between your staff and the support team at the core processing vendor, how they would describe their core conversion experience, what they learned in the process, what they’d do differently next time, and what they wish they had asked when they were choosing a vendor.

A: Although outsourcing your core can seem risky, there are many good vendors on the market, and some offer more than one product. These companies have been in business for a while, have plenty of customers like you, and understand FI needs. Be sure to vet the vendors on your shortlist very carefully, and seek consensus among your internal selection committee. And be prepared to use workload automation and orchestration as your safety net during the migration. These steps will help ensure your success. But if you’d like to make sure you can end the business relationship if needed, carefully inspect the opt-out language in your contract.

A: Although outsourcing your core can seem risky, there are many good vendors on the market, and some offer more than one product. These companies have been in business for a while, have plenty of customers like you, and understand FI needs. Be sure to vet the vendors on your shortlist very carefully, and seek consensus among your internal selection committee. And be prepared to use workload automation and orchestration as your safety net during the migration. These steps will help ensure your success. But if you’d like to make sure you can end the business relationship if needed, carefully inspect the opt-out language in your contract.

A: Some people will say everything is negotiable. And while that may technically be true, not every vendor is willing to make major changes to their standard contract. As you assess the offers, look at what components are most important and work harder on negotiating those. Include everything you’d like to negotiate, but make sure your list is prioritized so you focus on what really matters and make concessions on things that don’t matter as much.

A: Some people will say everything is negotiable. And while that may technically be true, not every vendor is willing to make major changes to their standard contract. As you assess the offers, look at what components are most important and work harder on negotiating those. Include everything you’d like to negotiate, but make sure your list is prioritized so you focus on what really matters and make concessions on things that don’t matter as much.

A: It is worth looking at different vendors every time your contract is up for renewal. You may find that your current vendor has new tools and support options that will help you continue to innovate, or you may find that a different vendor will give you better support and more flexible systems. If you are having problems with your current vendor and they aren’t able to resolve them reasonably, then check your contract for termination policies regarding failure to fulfill SLAs before making a change.

A: It is worth looking at different vendors every time your contract is up for renewal. You may find that your current vendor has new tools and support options that will help you continue to innovate, or you may find that a different vendor will give you better support and more flexible systems. If you are having problems with your current vendor and they aren’t able to resolve them reasonably, then check your contract for termination policies regarding failure to fulfill SLAs before making a change.

A: You may hear some of the core vendors mention that they use a public cloud. Public cloud is typically a shared cloud server, not a publicly accessible network, so they are likely to meet your minimum security requirements for third-party vendors. Because banking is such a highly regulated industry, any of the core vendors you look at will be able to provide their security information (and will be accustomed to fielding those questions). Public cloud can offer cost savings and scalability benefits with the same or higher security as a private cloud or on-premise system.

A: You may hear some of the core vendors mention that they use a public cloud. Public cloud is typically a shared cloud server, not a publicly accessible network, so they are likely to meet your minimum security requirements for third-party vendors. Because banking is such a highly regulated industry, any of the core vendors you look at will be able to provide their security information (and will be accustomed to fielding those questions). Public cloud can offer cost savings and scalability benefits with the same or higher security as a private cloud or on-premise system.

A: Outsourcing is not a fix-all. If your FI is committed to implementing new technologies for your customers and members, then you will want your core to allow you to do that. Many legacy, in-house core systems can make it challenging to integrate new functionality. If your core is flexible, you might be able to continue building new services around it. But if you find that you can’t do that easily, then outsourcing may be the solution you need. Just as important as the tool you choose, however, is the commitment to innovation at all levels within your FI.

A: Outsourcing is not a fix-all. If your FI is committed to implementing new technologies for your customers and members, then you will want your core to allow you to do that. Many legacy, in-house core systems can make it challenging to integrate new functionality. If your core is flexible, you might be able to continue building new services around it. But if you find that you can’t do that easily, then outsourcing may be the solution you need. Just as important as the tool you choose, however, is the commitment to innovation at all levels within your FI.

References

- Capgemini/EFMA, 2007 World Retail Banking Report

- Callahan & Associates, 2021 Supplier Market Share Guide: Credit Union Core Processors

- Celerity, What We Know Now: The State of Digital Transformation Today

- Capgemini/EFMA, 2020 World Retail Banking Report

- McKinsey & Company, Transforming Bank’s IT Productivity

- Capgemini/EFMA, 2021 World Retail Banking Report

- McKinsey & Company, What 800 Executives Envision for the Post-Pandemic Workforce

- Gartner, 2021 CIO Agenda: Seize This Opportunity for Digital Business Acceleration

- Research and Markets, Global Fintech Market, By Technology, By Service, By Application, By Region, Competition Forecast & Opportunities, 2026

- 1McKinsey & Company, AI-bank of the future: Can banks meet the AI challenge?

- Northeast Bank, Core Conversion Frequently Asked Questions

- Insight Credit Union, Core System Conversion: Frequently Asked Questions

- Dakota West Credit Union, Core Conversion FAQs

- Credit Union Times, Big Providers Still Dominate Core Provider Market, but Disruptors Lurk

- Aite Group LLC, AIM Evaluation: The Leading Providers of U.S. Core Banking Providers